by Amelia Tranter

In 2020, China’s ministry of agriculture and rural affairs explicitly stated that “with the progress of human civilisation and the public’s concern and preference for animal protection, dogs have changed from traditional domestic animals to companion animals”. This explicit statement marks a change in the way Chinese people own and nurture pets. As a result, China’s pet industry is entering a new phase of growth. The market has almost tripled in size over the last 5 years and is projected to grow even faster in the next five years. Societal shifts have given rise to a new generation of pet owners that are willing to spend more on their pets. The opportunities in the pet industry in the Chinese market are rife and in this report the key trends will be highlighted.

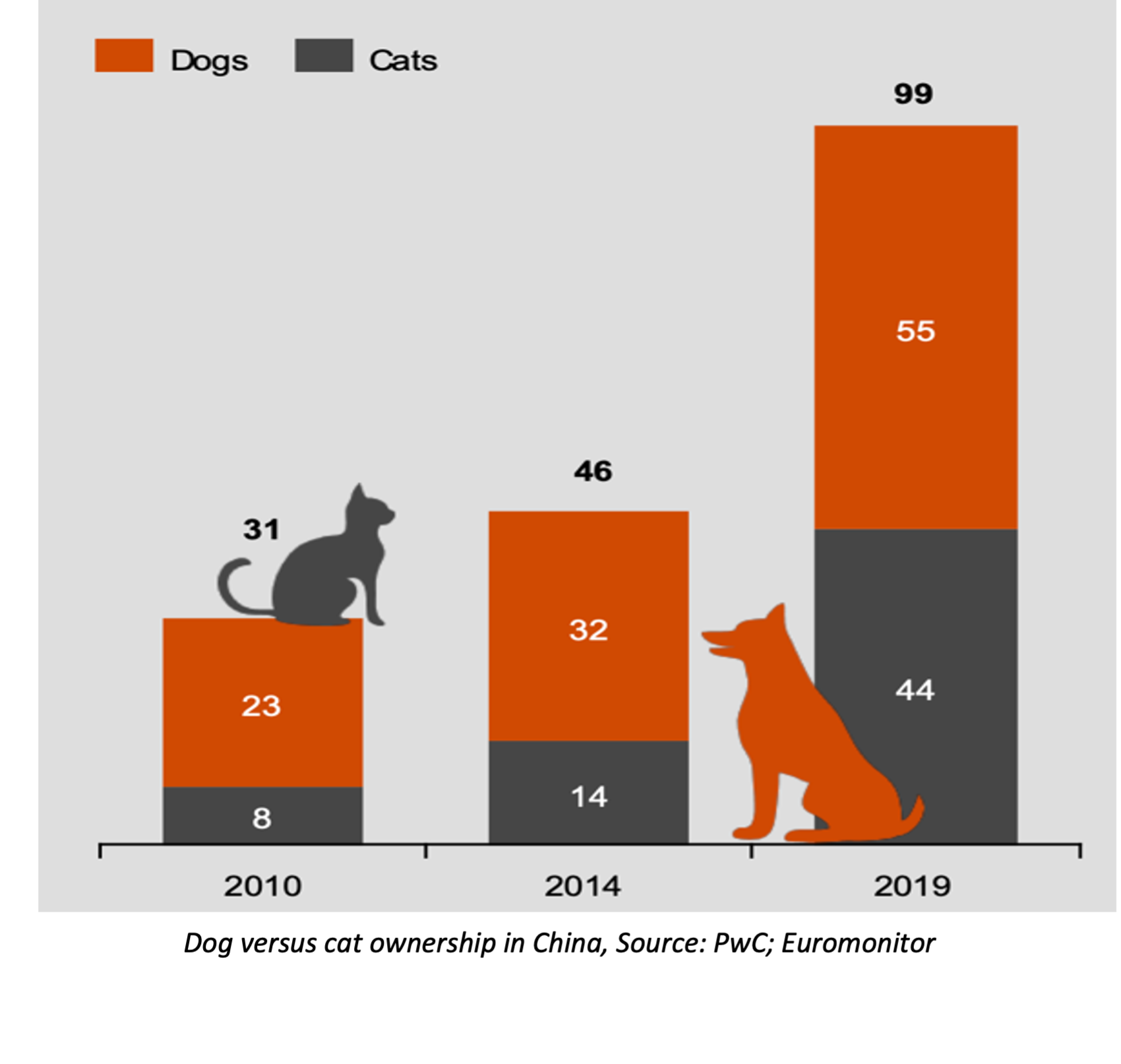

source: PWC; Euromonitor

Millennials are driving the pet economy

Behind this booming industry are Chinese millennials, with a total of 45.2% of all pet owners in China in 2019 being under the age of 30, and this number having increased proportionally more than any other age group. Whilst this age group are young, they should not be overlooked for the amount of money they are willing to spend on good quality products to ensure their pets are well-fed and healthy. The culture of caring for pets has evolved over the years. Whereas older generations may seek a pet for companionship, millennials consider themselves as parents to their pets and prioritise their pet’s welfare.

Another key characteristic of millennials is their aptitude and tendency to use social media. A recent Chinese trend called ‘cloud cat keeping’ (social media users can watch other people’s cats’ growth and progression online), has put pet ownership on an even higher social pedestal and is becoming an aspirational activity. The growth of ownership in this age category is strong and on the rise!

Cats vs. Dogs

Cat ownership has been growing at double the rate of dog ownership in China. Many urban Chinese youth are sharing viral cat photos, visiting cat cafes and also engaging in the aforementioned ‘Cloud cat keeping’, and this is leading them to want their own pet cat. The popularity of cats on the internet has given rise to a ‘cat-based economy’, a term coined by the Tencent Research Institute, describing the marketing power of cats towards young consumers. Chinese Millennials are considered “empty nest youth”; they work in large cities, far away from their families, and have relatively high disposable income. They often choose to raise cats as they are low maintenance pets that can live in apartments but also help to curb their loneliness from being away from their families.

The fact that there is a rise in popularity in cat ownership provides opportunities for brands which are in the premium and ultra-premium segment as cats have a stronger taste preference than dogs, meaning owners are more cautious about the products they choose for their pets. MNCs in this market have a distinct advantage over local players due to consumer perceptions of product quality being low for local firms. However, in the coming years, the MNC advantage is expected to reduce and this will not only open up opportunities for local firms, but also cross-border firms.

Pet Food is the primary driver of growth

The pet-food industry has the most immediate and attractive opportunities in the Chinese market. The pet-food industry comprises 55% of the overall China pet market, and has seen the strongest growth in recent times. With the new wave of younger pet owners and a shift towards seeing pets as one of the family, spending on pet-food has seen a significant rise and is remaining resilient throughout the economic downturn caused by the pandemic. Whilst the pet-food market is still generally dominated by MNCs, the competitive landscape in this industry is seemingly fluid and dynamic, creating opportunities for local players and also for more cross-border corporations and investors to break into the market.

Source: the happy cat site

Opportunities also extend to brands selling more premium pet-food alternatives. Whilst currently, premium pet-food only holds 3-5% of the whole Chinese market, some experts believe that it could be as high as 15-20% in top tier cities, where consumers are generally wealthier. Given the preference for cats over dogs, it is unsurprising that spending on cat and dog food is relatively even, despite cats being smaller in size and therefore having smaller food consumption. This is because there are more premium cat-food options on the market than there are for dogs. Whilst currently, ‘wet’ food for cats is still bought as a treat due to its higher price, the way the industry is growing, this is attitude is projected to change over time.

Digitally savvy shoppers looking for good quality pet products online

Over COVID-19 there has been an obvious need to place more emphasis on sales through e-commerce rather than through offline, physical channels. Within the pet food industry in China, e-commerce is the dominant channel, with 50% of pet food sales taking place online over offline channels like vet clinics, pet shops or supermarkets. China’s dominance in e-commerce is the highest that can be seen in the world, compared with 21% in the US and only 11% in Japan. The strong growth of ecommerce channels for purchases in the pet-food industry, combined with the well-developed e-commerce arena and high usage rate by consumers makes the Chinese market favourable for companies in the pet industry.

Whilst online markets can be associated with low-end and price sensitive customers, there is definitely space in the online sphere for ultra-premium products to be purchased, and in particular to find premium imported products. In 2018 it was reported that many online shoppers of pet products turned to cross-border e-commerce platforms to find premium quality imports that were not yet widely available offline in China. This was highlighted during 2019’s 11.11 shopping festival, an event that takes place yearly on Alibaba’s marketplace, Tmall Global. Canadian pet-food brands Orijen and Petcurean Go were among the top five selling brands across all categories on Tmall, and cat food was the top-selling category, out-performing other popular imported product categories like baby formula and skincare products.

Opportunities for products beyond a pet’s basic needs

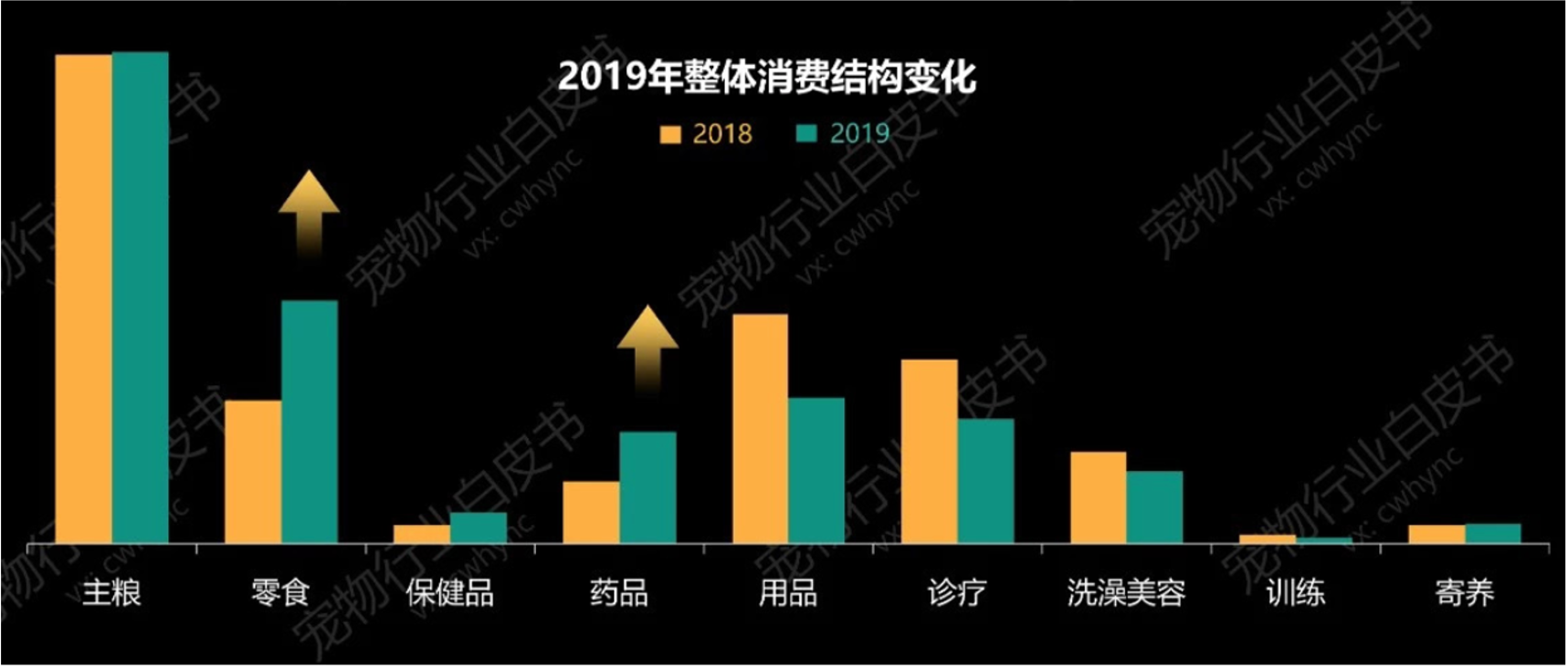

Chinese consumers, especially millennial pet owners, are willing to spend more money on their pets, purchasing non-essential items like fashion accessories and beauty products for them. Between June and December 2019, Tmall Global saw triple digit sales growth of pet grooming products like dry shampoos, paw lotions, eye serums and ear cleansers. Whilst the largest proportion of spending in the pet industry remains on food, the graph below also highlights the areas which are seeing significant growth.

Graph showing the change in the pet industry’s consumption composition (from left to right, staple food, treats, healthcare products, products e.g. toys or clothes, medicines, medical bills, grooming, training, catteries/kennels), source: 199IT

Treats is a relatively underdeveloped segment in China, but its share of the market has risen between 2018 and 2019, and is expected to rise significantly more as pet owners’ attitudes towards their pets and shopping habits change, meaning they choose to indulge their pets more often than before. Pet health supplements also grew by 50% year-over-year from 2017 to 2019. In general, demand for pet services is still centred around routinely medical check-ups at the vets, rather than non-essential services like catteries or kennels, training, grooming, photography and pet funerals, which are in the early stages of development in the Chinese market. Currently services only account for 25% of the pet market, but they have the potential to rise to somewhere between 35-50% like they are in more mature markets. As pet owners become more sophisticated and educated on the ways they can look after and nurture their pet, the demand for these services will undoubtedly rise.

Image 1: dog grooming services, source: petsitting lake mary | Image 2: Pet photography, source: Chinadaily

Let us help you

Visit our online marketplace to hire independent bilingual providers to get your bespoke projects done, or browse our comprehensive range of fixed price services that deliver the best value for money for your cross-border working. For specific enquiries, you can also contact us.