Driven by market opportunity, economic, energy and pollution concerns, China has invested nearly $900 billion in renewable power and fuels since 2009, more than double that of the US. China now possesses more than a third of the global solar and wind installed capacity, and leads the world in hydropower, lithium-ion battery supply chains, wind turbines, electric vehicle charging infrastructures, high-speed rails, and cleantech components manufacturing.

The West has also been making large investments in the battle against climate change and technology innovation. Most notably, US president Joe Biden committed more than $369 billion to subsidies and tax credits to encourage decarbonisation and cleaner energy. While in Europe, Ursula von der Leyen, president of the EU, announced the Green Deal industrial plan to counter the US and China in the cleantech battle. This raises the question: is China winning or losing the race in cleantech innovation?

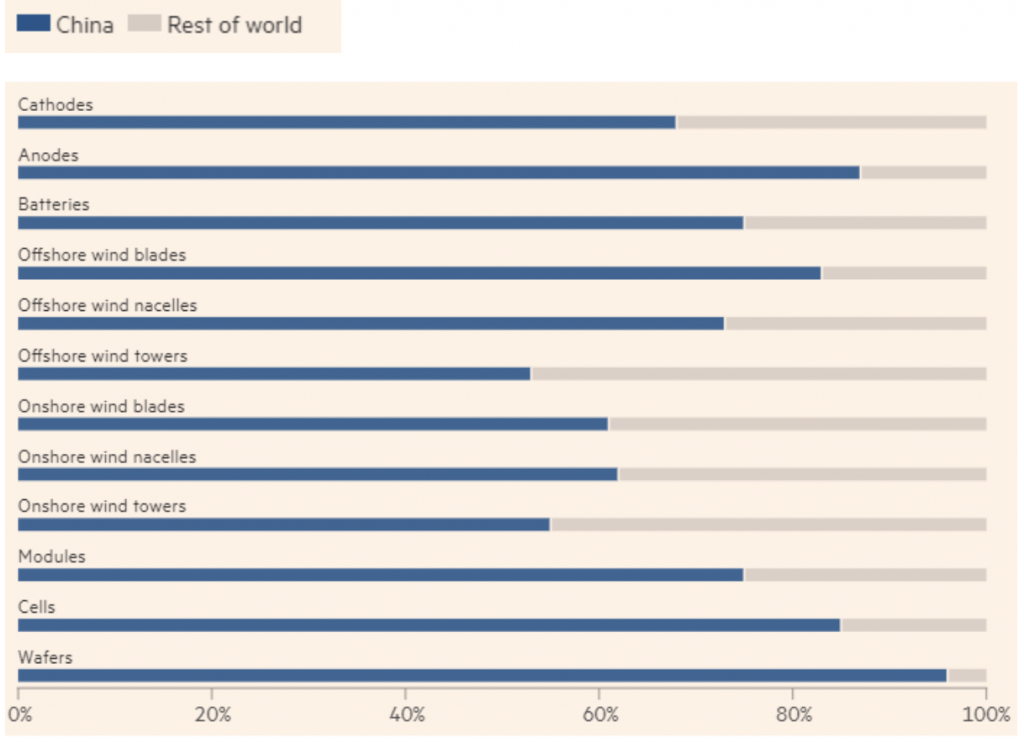

Production for Cleantech Components

Share of global manufacturing capacity by technology, 2021

The Four Key Areas of Competitive Innovation

Solar Power

The International Energy Agency has declared solar power to be the new ‘king’ of global electricity markets. In just over a decade, China has evolved into a world leader in solar power generation, despite previously lacking in this area compared to Western countries. China now has the world’s largest photovoltaic industry cluster, the largest application market, the most inventions and application patents, and is the largest investor in clean energy. China also has an estimated 2.7 million people employed in the solar energy sector, making up more than half of the world’s solar jobs.

Wind Power

Offshore and onshore wind power capacity is surging in China. For offshore wind, China now ranks third in terms of installed capacity, following the UK and Germany, even though its technology is less advanced than the West’s. Additionally, for ten consecutive years China has ranked number one in intellectual property competitiveness in offshore wind power and next-generation solar technology. Regarding China’s onshore wind capacity, one of the greatest developments has been the dramatic reduction in turbine prices, which have declined by 55-60% since 2010. It is now cheaper to build new wind or solar power generators than to continue to operate 60% of existing coal plants. China has also become the world’s largest wind power equipment manufacturing base.

Lithium-ion Batteries

China dominates the global market in terms of lithium-ion battery production. In the first quarter of 2022, China’s largest battery manufacturer, Contemporary Amperex Technology Co. (CATL), alone held around 35% of the global li-ion battery market. China also continues to invest heavily in R&D, including in alternative chemistries, in order to achieve further cost reductions and higher energy densities.

‘Green’ Hydrogen

‘Green hydrogen, which is produced using renewable energy, is a flexible and versatile breakthrough technology, with the potential to play an enormously important role in reaching net-zero emissions. China is the world’s largest producer of hydrogen, but most of it is ‘brown’ or ‘grey’ hydrogen produced from fossil fuels. China is aiming to increase its hydrogen production capacity to over 10 million tons by 2025 and over 20 million tons by 2030. This presents a significant opportunity for carbon capture, utilisation, and storage (CCUS) industries to provide carbon capture and storage solutions for hydrogen production.

China’s Climate Commitments

In September 2020, China made the commitment that it would peak its CO2 emissions by 2030 and aim to reach carbon neutrality by 2060. At the International Climate Ambition Summit in December 2020, China further committed to enhancing its Paris commitments by:

- reducing carbon intensity by over 65% by 2030 (compared to its initial Paris commitment of 60–65%)

- increasing the share of non-fossil energy in China’s energy mix to around 25% by 2030 (compared to 20% in its initial target)

- expanding total installed capacity of wind and solar to 1,200 gigawatts (GW) by 2030 (no previous target) (Schmidt et al, 2020)

These new 2030 commitments marked an important step forward. They were also a recognition of the immense economic potential in green energy innovation that drove China past its tipping point. The Chinese government has expressed strong support to reduce carbon emission and now provides a favourable policy environment for the growth of cleantech markets. There is a growing demand for clean energy solutions, including hydrogen fuel, which is likely to drive demand for solutions, such as CCUS, as it can help to make hydrogen production more environmentally sustainable.

In addition, China has also expressed its commitment to reducing its carbon footprint through the use of clean energy technologies and the implementation of carbon pricing mechanisms. China is investing vast resources into the development of clean energy, building facilities with new technologies and constructing clean, low carbon, safe and energy efficient systems to actively move towards a more sustainable system overall. The country is the largest domestic and outbound investor in renewable energy and cleantech solutions, which suggests a growing potential and demand for tech solutions, while also creating new business opportunities for companies in the sector.

Crayfish has recently included in its new strategic direction to support cleantech solutions, and commits to bridging the connection between innovative technologies and China. A number of projects are now underway.

HOW CRAYFISH CAN HELP

At Crayfish, we provide tailored solutions and are always happy to discuss ways to lead the way in China’s booming cleantech sector. Get in touch and book a free initial consultation with our specialist team.