Under the “dual carbon” goals, the Chinese government is actively promoting the development of new energy vehicles (NEVs) towards intelligence and connectivity, supported by continuous policy initiatives and technological innovations. The NEV market in China is predominantly led by battery electric vehicles (BEVs), while the share of plug-in hybrid electric vehicles (PHEVs) has been steadily increasing year by year. Additionally, the rapid expansion of charging infrastructure has significantly improved the convenience of electric vehicle (EV) usage. These factors have collectively accelerated the growth of China’s EV industry, injecting new momentum into the sector’s development.

Policy support

China has introduced several measures to accelerate the development of new energy vehicles (NEVs), such as relaxing NEV purchase restrictions, offering subsidies for old vehicle replacement, and providing tax exemptions. These measures are expected to further stimulate the NEV sector and contribute to the country’s carbon reduction goals.

In June 2023, the General Office of the State Council issued the Guiding Opinions on Further Building a High-quality Charging Infrastructure System This policy aims to build a charging infrastructure system by 2030 that features extensive coverage, appropriate scale, optimal structure and comprehensive functionality, supporting the development of new energy vehicles while meeting the public charging needs. The goals include building a charging network with strategically placed stations in urban areas, along major roads and in rural regions. This plan aims to gradually increase the coverage of charging services in rural areas, creating a comprehensive system that covers both urban and rural communities.

In terms of tax support policies, measures implemented from January 1, 2024, include exemptions from vehicle purchase tax for new energy vehicles (NEVs) purchased between January 1, 2024, and December 31, 2025, with a cap of 30,000 yuan per vehicle. For NEVs purchased between January 1, 2026, and December 31, 2027, the vehicle purchase tax will be reduced by 50%, with a cap of 15,000 yuan per vehicle.

Aligned with advancements in NEV technology, China has updated the technical requirements for vehicle purchase tax exemptions. Starting from January 1, 2024, models listed in the Catalog of New Energy Vehicle Models Exempt from Vehicle Purchase Tax by December 31, 2023, and still valid, will be automatically transferred to the Catalog of New Energy Vehicle Models Eligible for Tax Reduction or Exemption.

In April this year, the Ministry of Commerce, along with six other departments released the Implementation Rules for the Subsidy for Old-for-New Vehicles, This initiative offers subsidies for consumers who scrap old vehicles and purchase new ones. A subsidy of 10,000 yuan is offered for purchasing an NEV. Subsequently, the Ministry of Finance issued the Notice on the Budget for the Central Government’s Pre-allocated Funds for the Subsidy for Old-for-New Vehicles in 2024, announcing a pre-allocation of nearly 11.2 billion yuan in central government subsidy funds to various provinces, regions, and cities. This initiative aims to further stimulate automobile consumption by supporting the scrapping and replacement of old vehicles that meet subsidy policy requirements, with a focus on enhanced standards for technology, energy efficiency, and emissions.

In May, the State Council issued the 2024-2025 Energy Conservation and Carbon Reduction Action Plan, which explicitly calls for accelerating the low-carbon transformation of transportation equipment. Key measures include eliminating old vehicles, raising the energy consumption standards for operating vehicles, gradually lifting restrictions on the purchase of new energy vehicles (NEVs), implementing policies to facilitate the use of NEVs, and promoting the electrification of public sector vehicles. The plan also aims to promote the adoption of new energy medium- and heavy-duty trucks, establishing zero-emission freight fleets, and intensifying efforts to advance energy conservation and carbon reduction to achieve the carbon peak and carbon neutrality goals.

At the same time, the initiative to promote new energy vehicles in rural areas, known as “going to the countryside”, has been launched to further stimulate demand in rural markets, creating a dual benefit alongside the old-for-new policy.

In addition, local policies are actively promoting NEV consumption. For example, Shenzhen has eased the requirements for purchasing NEVs, including removing social security restrictions for non-local residents and optimizing the conditions for applying for NEV purchase quotas.

In September 2024, the National Development and Reform Commission (NDRC) and three other departments jointly launched a pilot program for large-scale interactive applications of electric vehicle networks. The goal is to promote deep collaboration between NEVs and the power grid, optimize the allocation of charging resources, support the achievement of the “dual carbon” goal, and promote the coordinated development of NEVs and the electricity market.

At the same time, the Ministry of Transport, in collaboration with several departments, issued the Measures to Accelerate the Enhancement of Lithium Battery Transport Services and Safety Assurance Capabilities for New Energy Vehicles, aiming to improve the safety, efficiency, and convenience of lithium battery transportation. This is expected to support the high-quality development of the NEV and lithium battery industries and assist the construction of a modern industrial system and the development of new productive forces.

The Market Data

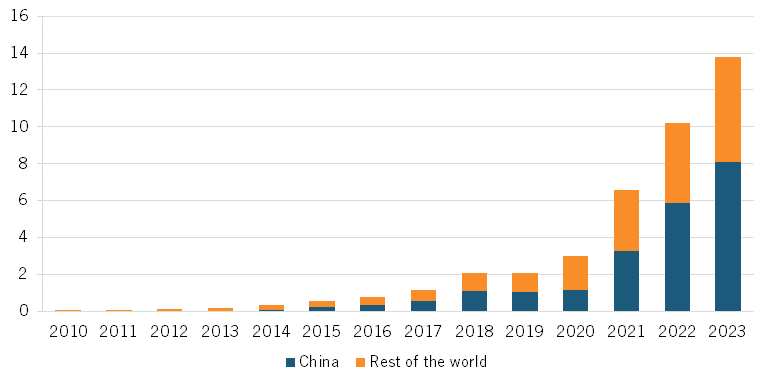

Chinese enterprises have emerged as dominant players in the global electric vehicle (EV) industry. By 2022, Chinese manufacturers accounted for 62% of global EV sales, a remarkable leap from just 0.1% in 2012. In 2023, approximately 6.69 million battery-electric vehicles (BEVs) were sold in China, reflecting a 24.63% increase compared to the previous year. Additionally, around 2.8 million plug-in hybrid electric vehicles (PHEVs) were sold, bringing total EV sales to over 9.4 million.

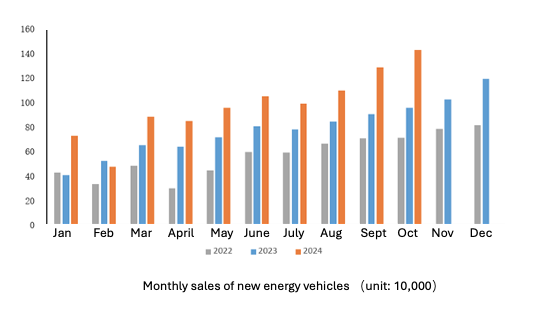

According to the China Association of Automobile Manufacturers (CAAM), from January to October 2024, the production and sales of new energy vehicles (NEVs) reached 9.779 million and 9.75 million units, respectively, representing year-on-year increases of 33% and 33.9%. In October, NEVs continued to experience rapid growth, with monthly production and sales hitting new highs, reaching 1.463 million and 1.43 million units, respectively, showing year-on-year growth of 48% and 49.6%.

In October, the overall performance of new energy passenger vehicle companies remained strong. BYD’s pure electric and plug-in hybrid vehicles further solidified the leading position of domestic brands in the NEV market. Extended-range electric vehicles, represented by companies such as Li Auto, Seres, Changan Automobile, and Leap Motor, continued to perform strongly. In October, the production of new energy passenger vehicles reached 1.379 million units, reflecting a year-on-year increase of 49.9% and a month-on-month increase of 12.6%. From January to October 2024, production totalled 9.244 million units, marking a year-on-year increase of 35.2%.

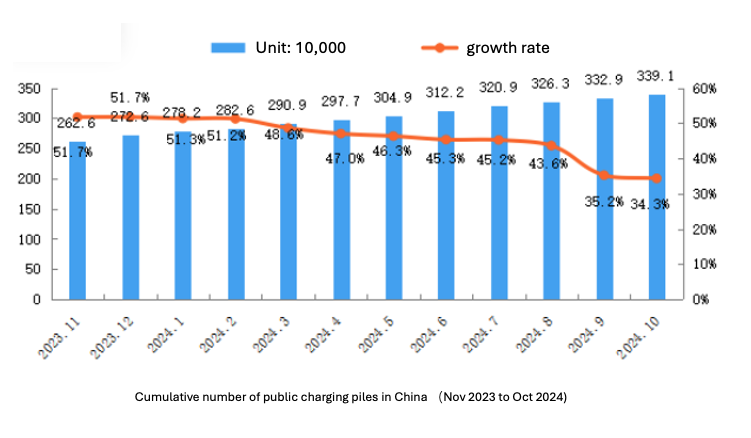

The China Charging Alliance (CCA) released the national electric vehicle (EV) charging and swapping infrastructure operational data for October 2024. In October 2024, the number of public charging piles increased by 63,000 compared to September 2024, representing a growth of 34.3%. As of October 2024, the member organizations of the CCA reported a total of 3.391 million public charging piles, including 1.535 million DC charging piles and 1.855 million AC charging piles. From November 2023 to October 2024, an average of approximately 72,000 new public charging piles were added each month.

From January to October 2024, the increase in charging infrastructure reached 3.288 million units, reflecting a year-on-year increase of 19.8%. The increase in public charging piles was 665,000 units, a decrease of 8.6%, while the increase in private charging piles installed with vehicles was 2.623 million units, marking an increase of 30.1%. As of October 2024, the total number of charging infrastructure units nationwide had reached 11.884 million, reflecting an increase of 49.4%.

We follow closely the trends and developments in the EV industry in China and worldwide. Read here to find out more:

- What splashes have China’s car industry and EV makers like BYD made in global media? And the most valuable Chinese brands in 2023 are…

- Chinese EVs and a 100% US tariff got the EU and UK worried, but why? If the EV phenomenon is only the tip of the iceberg, what is beneath?

- Chinese EV speeds ahead: domestic booms, shifting global landscape, challenges and considerations

Advantages of China’s EVs

China’s electric vehicle (EV) industry has seen rapid growth, achieving remarkable advancements in battery technology, vehicle design, and autonomous driving capabilities. Companies such as Gotion and SVolt operate large-scale, highly automated production facilities, focusing on diverse battery chemistries and innovative technologies like solid-state and sodium-ion batteries. These innovations have greatly improved EV affordability, safety, and range, strengthening their global competitiveness.

Chinese automakers leverage artificial intelligence to develop smart cockpits and advanced driver-assistance systems (ADAS), prioritizing software and user experience to differentiate their offerings. The widespread adoption of cost-efficient lithium iron phosphate (LFP) batteries, which power two-thirds of EVs in China, along with emerging sodium-ion technology, has further reduced costs and decreased reliance on critical minerals.

China also leads the global EV battery industry, supported by robust research, high-impact patent output, and strategic control of raw materials. Key breakthroughs include CATL’s “Shenxing Plus” LFP battery with a 1,000km range, and Nio’s semi-solid-state batteries offering industry-leading energy density. Global automakers like Ford and GM are licensing these advanced technologies, cementing China’s position as a global leader in EV innovation. These advancements, paired with modern designs and competitive pricing, are driving global demand for Chinese EVs while reshaping the automotive landscape.

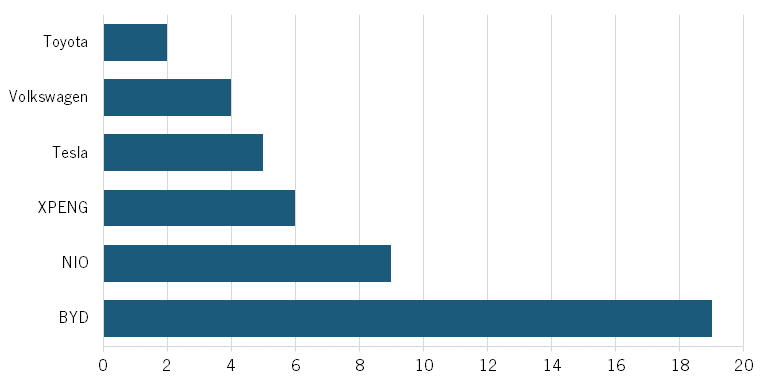

Chinese EV makers excel in process innovation, operating more like agile startups than traditional automakers. They are approximately 30% faster in vehicle development compared to legacy manufacturers, leveraging streamlined practices free from the constraints of combustion-engine production. From 2017 to 2023, Chinese brands introduced significantly more new EV models, with BYD releasing 19, Nio 9, and XPeng 6, far outpacing Tesla (5), Volkswagen (4), and Toyota (2). This rapid pace highlights their competitive edge in innovation and market responsiveness. (See figure.)

Trends and Dynamics in China-UK Collaboration

The world automotive industry is undergoing a phase of multi-technology innovation and cross-industry integration, with accelerated convergence between automobiles and energy, transportation, information technology, and urban systems. Electrification, intelligence, connectivity, and sustainability have become key drivers for the industry’s transformation and development.

In May 2023, the World Economic Forum projected that global electric vehicle sales would need to increase 18-fold by 2030 to meet global emission reduction targets. Achieving this goal will require concerted efforts across the global automotive industry, including optimising supply chains and fostering international collaboration. Both China and the UK, as major players in the automotive industry, must intensify efforts to drive innovation, production, and adoption of EVs to meet this demand.

The UK’s decision to phase out new gasoline and diesel vehicles by 2030 and mandate zero tailpipe emissions by 2035 aligns with global efforts to reduce carbon emissions. This regulatory shift sends a clear signal to the industry to accelerate EV production, creating opportunities for collaboration with countries like China.

China is emerging as a hub for innovation in intelligent and connected vehicles, with rapid advancements in both hardware systems and software technologies. At the World New Energy Vehicle Congress in September 2024, participants highlighted ongoing breakthroughs in electrification, intelligence, connectivity, and sustainability within the new energy vehicle sector.

China’s Ministry of Industry and Information Technology emphasised leveraging international cooperation to drive innovation in the automotive industry, enhance technical capabilities, refine carbon emission standards, and promote the integration of the automotive sector with the energy and transportation industries to achieve a low-carbon transformation. Experts at the event stressed the importance of lightweight vehicle design, comprehensive application of intelligent technologies, and global policy coordination and supply chain collaboration to address industry challenges and build a green, low-carbon, and sustainable global automotive ecosystem.

Chinese electric vehicle brands, particularly BYD and Xpeng, have begun entering the UK market. In March 2023, BYD officially launched its ATTO 3 electric SUV in the UK. More recently, in addition to established brands like BYD and Xpeng, Leapmotor, a China-Italy joint venture, has also included the UK in its global expansion plans.

In March, The Guardian reported that Chinese battery manufacturer EVE Energy plans to invest £1.2 billion in a gigafactory in Coventry, UK. Once completed, the factory is expected to produce 60 GWh of batteries annually, enough to power 600,000 electric vehicles. This investment is poised to further drive the development of the UK’s electric vehicle industry, offering both innovation and cost-reduction benefits.

At the International Investment Summit held in October, the UK government announced £63 billion in private investment, including funds allocated to green infrastructure projects such as data centres, offshore wind power, and carbon capture and storage. These large-scale investments in green infrastructure and the UK’s push for net-zero emissions create substantial business opportunities for both the UK and China in the EV and green energy sectors. The two countries can collaborate across various fronts—renewable energy, AI, carbon capture, and data-driven solutions—to accelerate EV adoption, reduce emissions, and build a sustainable future. From joint ventures in clean energy to advancements in smart transportation technologies, these developments open a wide range of opportunities for UK-China business growth in the green economy.

Furthermore, despite the United States and the European Union imposing punitive tariffs on imported electric vehicles from China, the UK, no longer bound by EU trade policies, has adopted an independent approach. Chancellor of the Exchequer Rachel Reeves emphasised that any decisions regarding EV tariffs must strike a balance between protecting the UK’s domestic EV industry and maintaining trade relations with China. This independent stance suggests greater potential for China-UK cooperation in the EV sector in the future.

As UK-China cooperation in green technology deepens, the electric vehicle industry has become a strategic focal point for bilateral collaboration. Both countries are leveraging their respective strengths and resources to establish mutually beneficial partnerships in the EV market, with a particular focus on areas such as battery technology, autonomous driving, charging infrastructure, smart grids, and supply chains.

Cross-border investment decisions require a comprehensive consideration of both macro and micro factors, as well as a balance between the bigger picture and finer details. Whether UK businesses are expanding into the Chinese market or Chinese companies are entering the UK, leveraging reliable professional consulting and business services can significantly enhance the likelihood of success.

For Chinese companies seeking to enter the UK electric vehicle market, or UK companies aiming to tap into the Chinese EV market, whether you are looking for high-quality investment opportunities, assistance with bidding, professional due diligence, financing advice, or support with corporate restructuring, Crayfish is here to provide expert assistance. Please feel free to contact us.

Whether you are looking for distributors, manufacturing & sourcing partners or investors, you can find more information and/or services that may just be what you need 👇